Contributor: Scott Warren

Businesses don’t always have a choice in their level of cash reserves, but having a target will help guide decisions regarding how to deploy cash. Deciding what that target should be depends on your business’s particular risk factors. There is no exact formula, but consider the two broad categories of revenue generation and fixed vs. variable expenses as a starting place and a range of three to six months of operating expenses for your cash reserve. If your risk in generating stable income and your fixed costs are both high, your cash reserve target should be closer to six months.

Try the following approach to get a sense of what type of cash reserve target you should have.

1. Start your analysis by identifying and assessing your revenue risks. These risks could include factors such as:

a. Diversity of revenues – Greater diversity equals lower risk. Consider various types of diversity, including industry, size of company, location, etc.

b. Concentration of revenue – This is the flip side of diversity of revenues. If a large percentage of your revenue comes from one source, your risk is higher.

c. Margin associated with revenue line items – Greater margins equal lower risks.

d. Control over revenue – Is your product or service necessary or optional for your customers?

e. Length of contracts – Do you have contracts? Do they span months / years? What are the terms of cancellation?

f. Market share – How likely is it that your organization will be on the “short list” as customers make their decisions.

g. Economy – How is the economy – local, national or international – based on where you draw customers?

h. Trends – Does your crystal ball show that things are getting better or worse?

i. Accounts receivable – Are you a cash business? Will you be able to collect your accounts receivable?

2. Next, identify and assess your fixed versus variable costs. More fixed costs mean higher risk because you cannot make adjustments as quickly and, therefore, a higher cash reserve target is appropriate. Consider:

j. Type of expense – Examine your fixed short-term vs. long-term expense commitments.

k. Debt service – How much do you have to pay to stay current, and what is that as a percentage of total expenses?

l. Long-term leases – Again, what are the fixed payment commitments?

m. Staff – Can you cut staff if you lose contracts? How fast are you willing to cut staff if there’s a downturn?

n. Corporate overhead – What other overhead costs are essentially fixed?

o. Variability of expense – Examine the flexibility of expense levels for different business units.

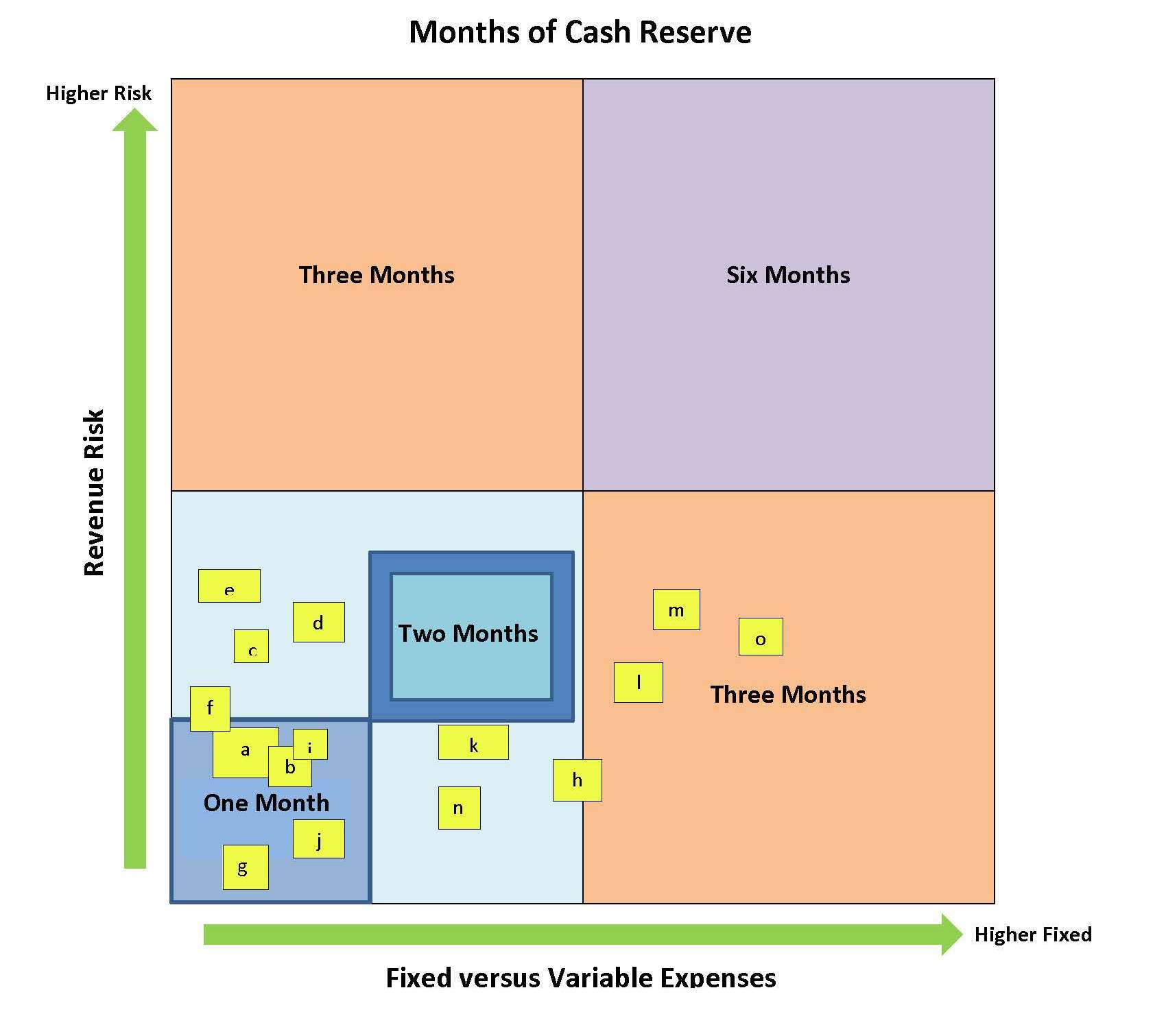

3. Finally, plot your risk assessment on a matrix where one axis represents revenue risks and the other represents fixed cost risks. See an example below.

Example of Completed Cash Reserve Matrix

Suggesting a Reserve Equal to Two Months of Expenses

(letters indicate risk factors listed above)

This methodology should provide structure to support to your estimation of cash reserves.